December 26, 2023

HAPPY NEW YEAR!!! Now, what does that mean for

Orange County real estate?

First, let us look back at what happened in 2023 in terms

of inventory, demand, luxury properties, and the

Expected Market Time.

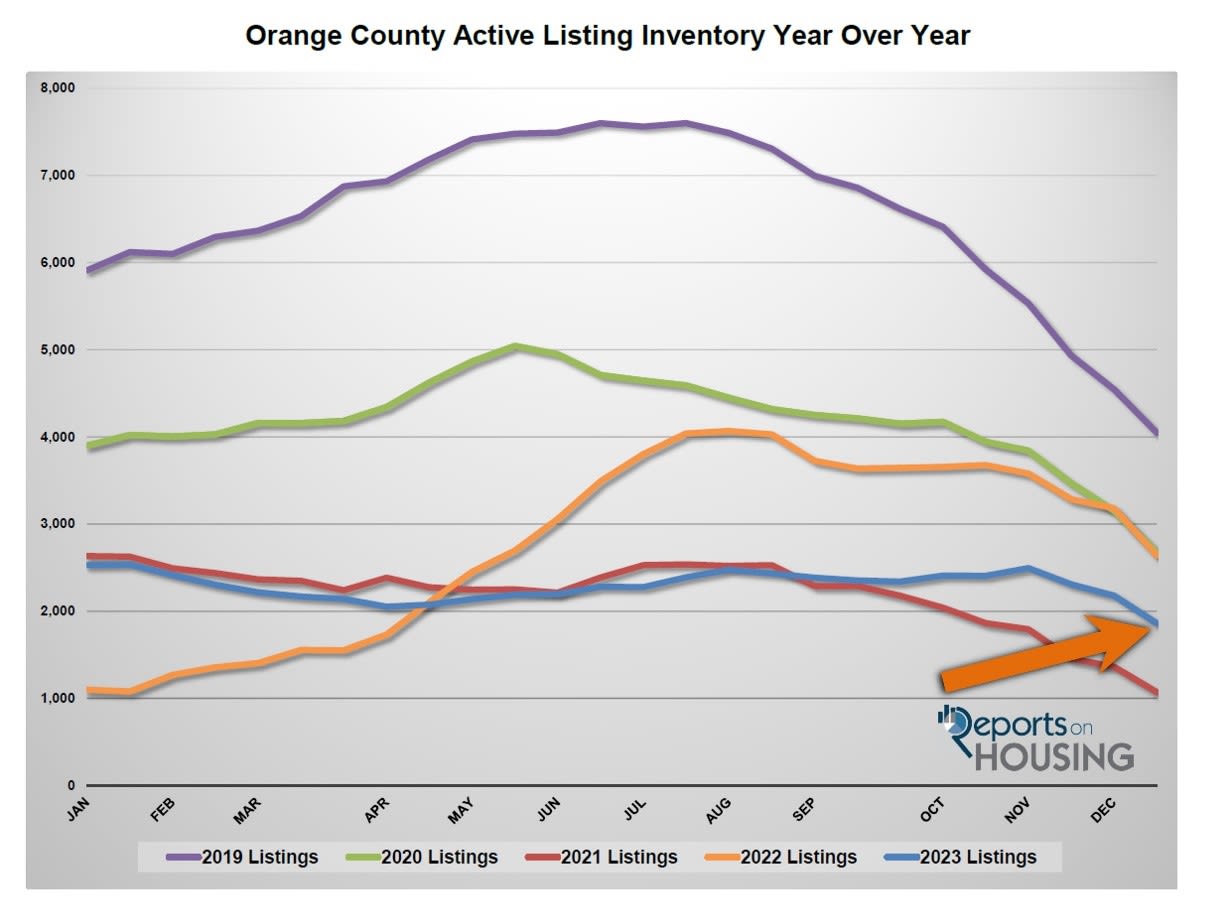

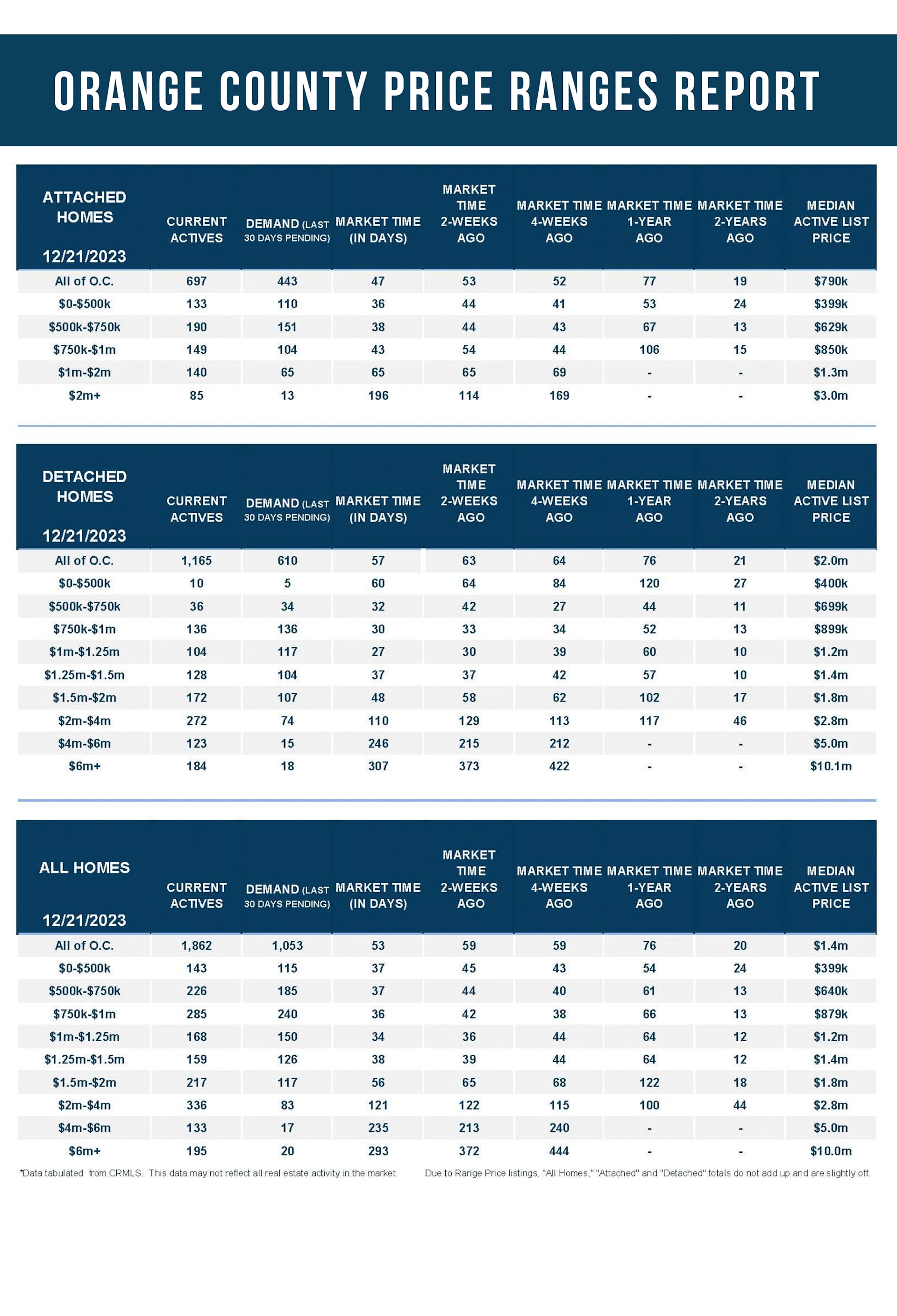

Active Inventory

The inventory remained extremely low all year and did not eclipse January levels.

The year started with an active inventory of 2,431 homes, the second lowest level to start a year since tracking began in 2004, only behind 2022’s 954 anemic start. The average start before the pandemic was 4,500 homes, a revealing 85% higher. A lack of available homes to purchase has been the mantra for the housing market since the pandemic hit nearly four years ago. After reaching 2,536 homes in mid-January, the inventory did not rise until the end of April after dropping to 2,053, down 19%.

It appeared that Orange County was going to hit its peak at the beginning of August at 2,475 homes; but, with rates stubbornly remaining above 7% since July and even eclipsing 8% in October, the peak was not reached until the start of November at 2,496 homes, growing by 21% since April. The 3-year average peak before COVID (2017 to 2019) was 6,959 homes, 179% higher than this year. From November through year’s end, the number of available homes decreased to 1,862, an unprecedented low level only surpassed by the end of 2021’s 1,072 level. The end to 2023 was 58% below the 3-year average end to December of 4,479.

During the Holiday Market, as rates dropped below 7% for the first time since July and hit levels last seen in May at 6⅔%, the inventory dropped by 634 homes in the last six weeks of the year, down 25%. The inventory is poised to drop below 1,700 upon ringing in a New Year, a depleted number of available homes.

COVID suppressed the inventory in Orange County in 2020 and 2021. There were 5% fewer homes placed on the market in 2020 compared to the 3-year average before COVID (2017 to 2019), and 6% fewer in 2021, or 2,311 missing sellers. In 2022, due to skyrocketing mortgage rates, homeowners opted to stay put and “hunker down,” enjoying their fixed, low monthly mortgage payments. A remarkable 85% of California homeowners with a loan enjoy a fixed rate at or below 5% (Q3-2023). 68% are at or below 4%, and 30% have a rate at or below 3%. There were 22% fewer homes placed on the market in 2022 compared to the 3-year average, 8,450 less. This trend grew significantly as 2022 progressed, and rates eclipsed 7% in October and November 2022. In 2023, the trend continued where 2022 left off, and homeowners hunkered down all year. Through November, there were 41% fewer FOR-SALE signs, 15,583 fewer.

The inventory crisis deepened, not because of excess demand, but due to homeowners continuing to “Hunker Down.”

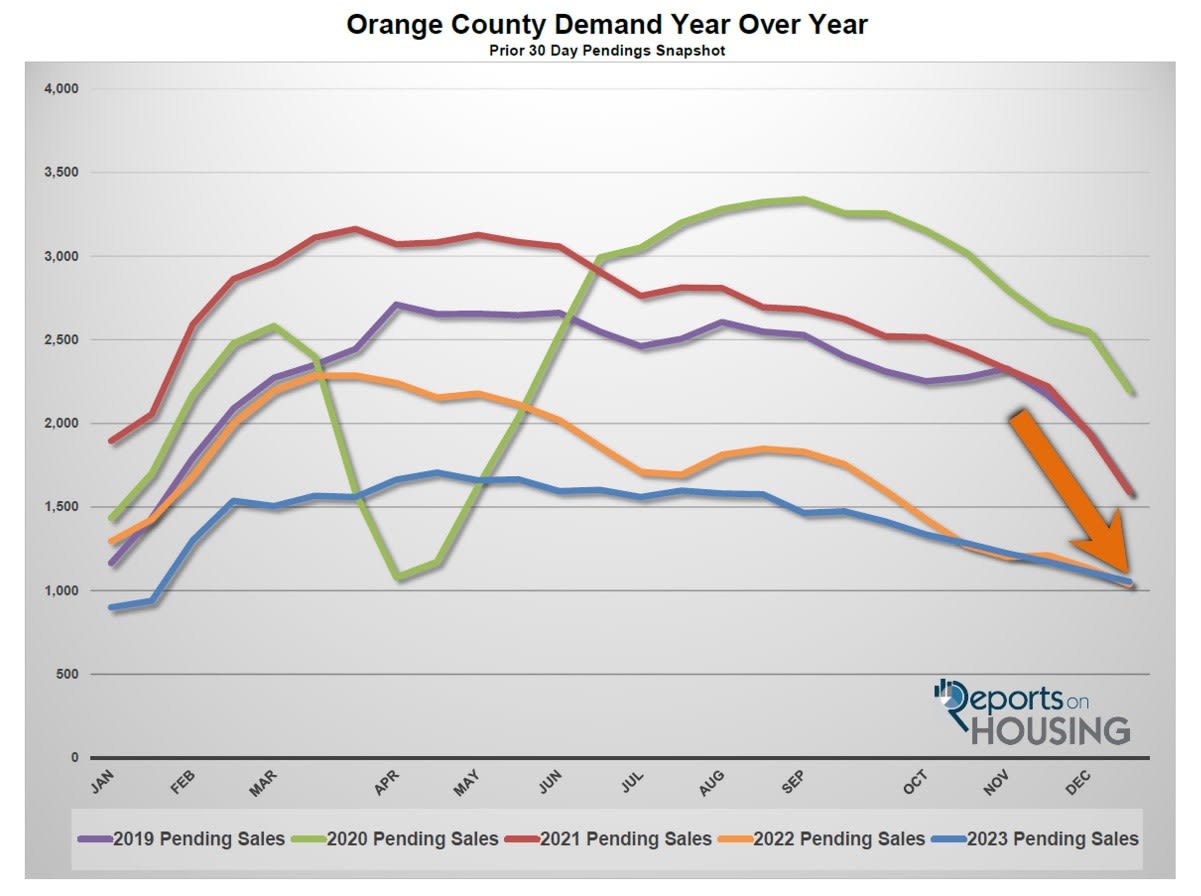

Demand

Demand hit lows that dropped below Great Recession levels.

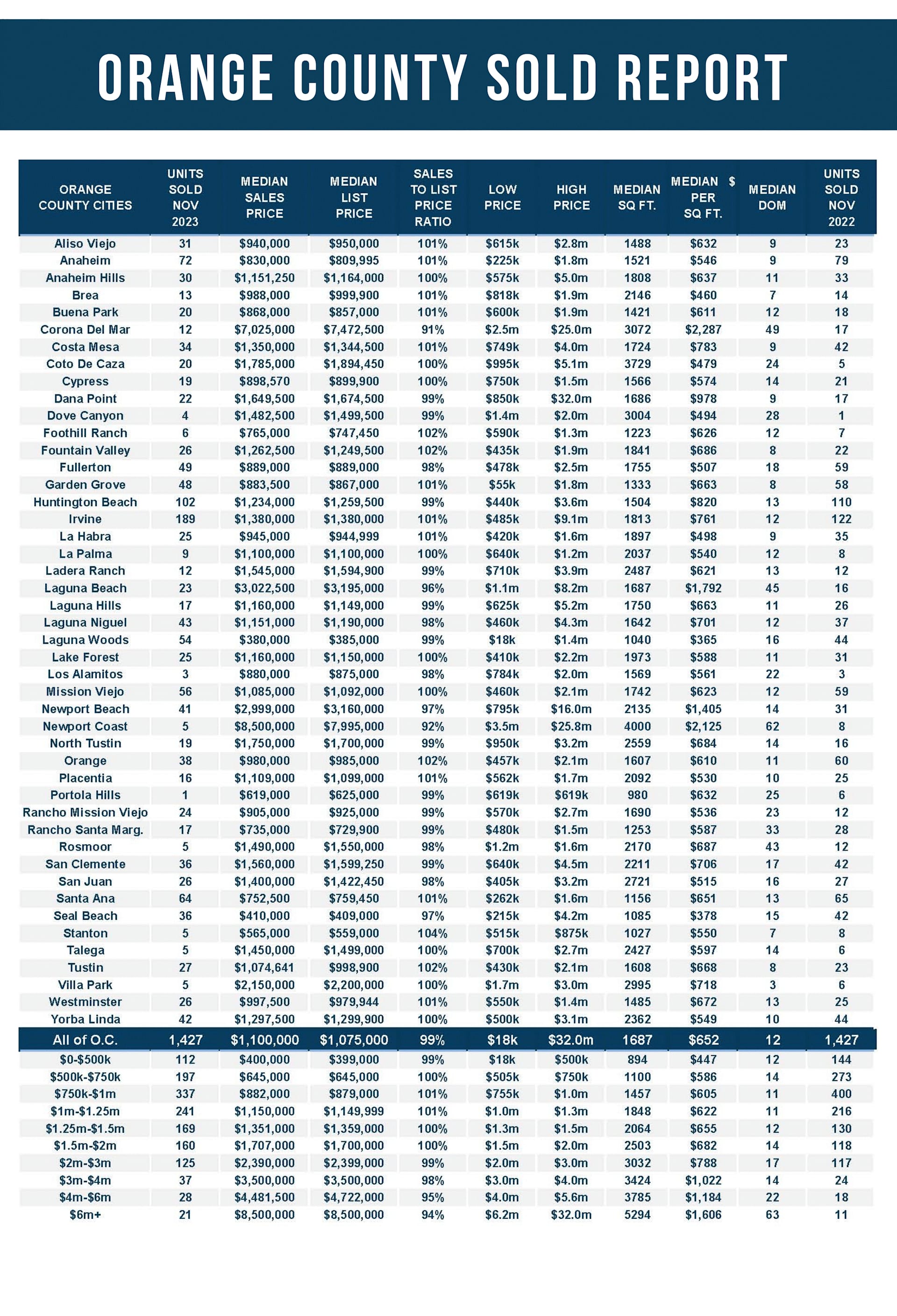

Demand for Orange County homes (a snapshot of the number of new pending sales over the prior month) followed the typical seasonality pattern but was severely muted all year. The Spring Market was the strongest, followed by the Summer Market, Autumn Market, and, finally, the Holiday Market. This seasonal pattern mirrors when homes are placed on the market. Even though fewer homeowners opted to sell, the most came on during the spring, and the least came on during the holidays.

At the beginning of the year, demand for Orange County homes (the number of pending sales over the prior month) was muted compared to 2022, down 31%, and down 35% compared to the 3-year average before COVID (2017 to 2019). Demand was muted because higher rates severely impacted home affordability. In looking at mortgage rates, home values, and household incomes, affordability reached historic lows. The lack of homeowners opting to sell contributed to the low demand readings. There was a scarcity of homes available in most price ranges throughout the year. Housing was still hot despite the lack of pending sales.

After starting the year at 888 pending sales, demand peaked at the end of April at 1,706, its lowest peak since tracking began in 2004. It was 25% lower than 2022’s 2,286 peak and 39% below the 3-year average peak before COVID (2017 to 2019) of 2,816. Demand was flat all year but dropped substantially from the end of July to the start of the Holiday Market in mid-November due to rates remaining above 7% and surpassing 8% in October, plunging by 23%.

Within the past four weeks, demand dropped by 120 pending sales, or 10%, and now sits at 1,053 pending sales, the lowest reading since January. At the end of December 2022, demand was at 1,038 pending sales, or 1% lower. It was the lowest end-of-the-year reading since tracking began in 2004. The 3-year average end to December before COVID was 1,499 pending sales, or 42% higher.

Luxury End

The luxury home market was down 19% through November 2023 compared to 2022.

2021 was a record-setting year for luxury sales above $2 million in Orange County, eclipsing the prior year by 88%. Despite higher rates, 2022 was the second strongest, 14% lower than 2021. Through November, 2023 was off by 19% compared to the previous year and 28% compared to 2021. It is still the third strongest year for home sales above $2 million since tracking began in 2004.

In the first quarter of 2023, there were 39% fewer luxury sales year over year. The second quarter of 2023 was down 32%. It was down by 5% during the third quarter but up by 35% in the fourth quarter.

During the pandemic, the luxury market evolved to an incomprehensible fast pace. Luxury homes that typically took months to sell were selling almost instantly. In February 2022, the Expected Market Time (the time between coming on the market and opening escrow) reached a record low of 45 days. That changed as rates rose and equity market volatility became the norm. In 2023, luxury decelerated quite a bit from the accelerated pandemic pace. In April, the Expected Market Time dropped to 101 days for homes priced above $2 million. It grew to 140 by the end of August and stretched to 168 days at the start of December.

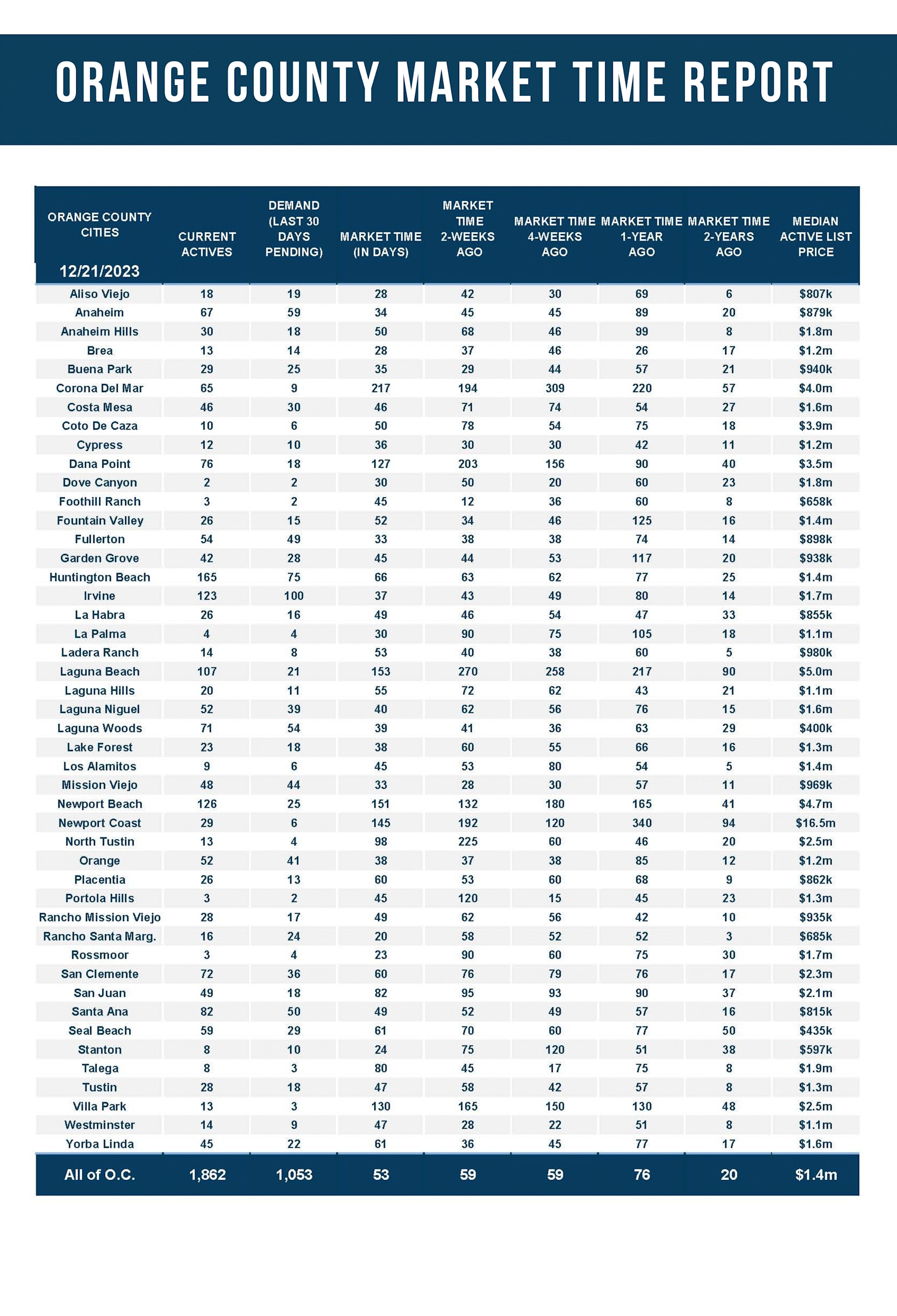

As of the end of December, luxury demand is at 120 pending sales, 6% higher than 2022. The inventory is at 664 after plunging by 11% in the previous two weeks, 20% higher than 2022. The expected market time for luxury finished the year at 166 days.

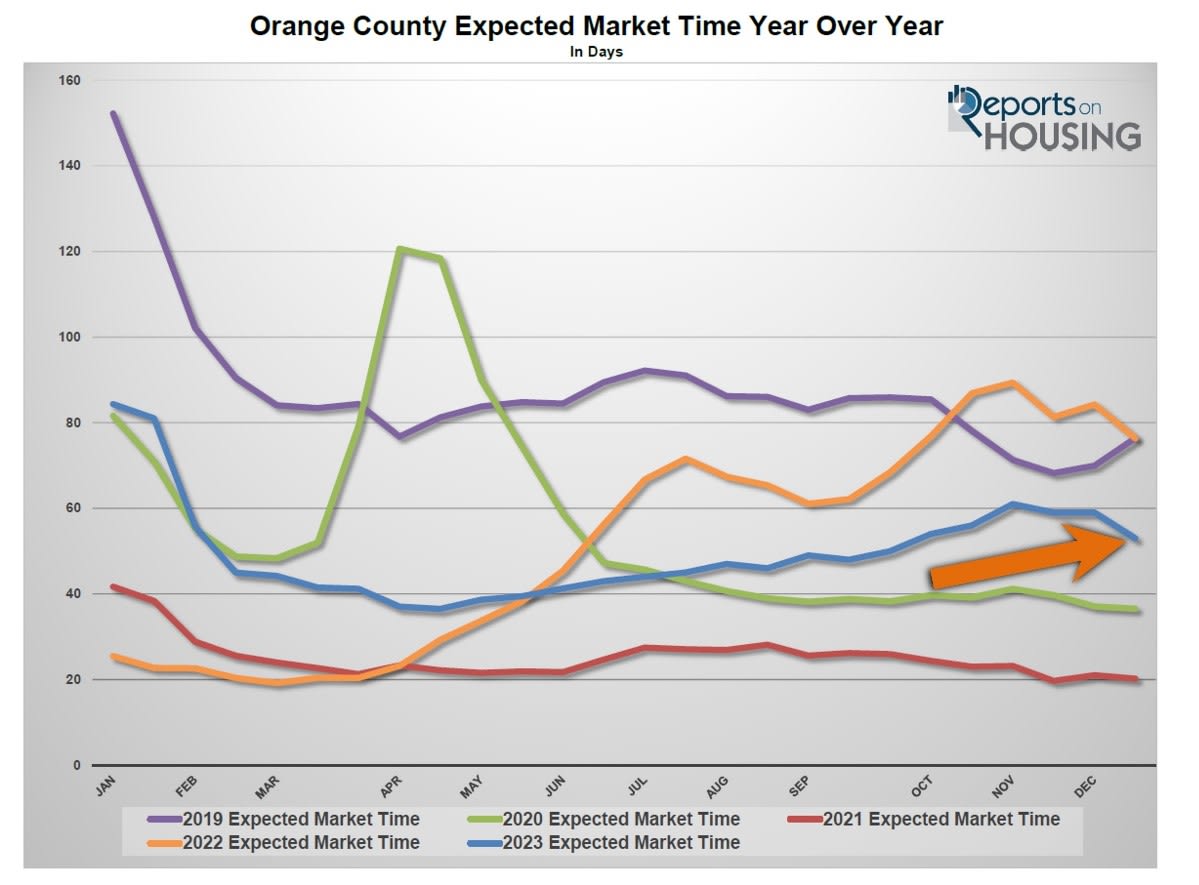

Expected Market Time

The time it took to sell a home grew longer as the year progressed.

The Expected Market Time, the amount of time it would take to place a home listed today into escrow down the road (based upon current supply and demand), started the year at 82 days, very similar to pre-pandemic levels. Yet, rates dropped quite a bit at the start of 2023 and even hit 5.99% on February 2nd. By the end of April, the Expected Market Time dropped to 37 days, an insanely hot market that heavily favored sellers, similar to the COVID years from June 2020 through May 2022. Homes were flying off the market, and buyers were willing to pay over the asking price to obtain a home.

Yet, the Expected Market Time grew as mortgage rates climbed and remained above 7% from July through mid-December. It surpassed 50 days in September and eclipsed 60 days in November. With rates dropping below 7% at the end of the year as the Federal Reserve signaled that there would be three rate cuts in 2024, the market time retreated to 53 days by year’s end. In the past two weeks, the Expected Market Time for Orange County dropped from 59 to 53 days, substantially lower than 2022’s 76 days to end the year.

The 2024 Forecast

Housing starts to thaw.

After reaching a record peak in May 2022, home values dropped through December, seven straight months of dropping prices. Yet, the inventory of available homes sank to start the year as rates dropped from their end-of-the-year 2022 highs. Home affordability improved slightly as the scarcity of homes available dropped to problematic, low levels, especially in the lower price ranges. The muted supply overshadowed the affordability predicament, and home values rose throughout 2023, surpassing the May 2022 height. The Federal Reserve raised the Federal Funds Rate from 0 to 4.5% in 2022 and hiked it to 5.5% in 2023. Inflation eased from 6.4% in December 2022 to 3.1% in November 2023. Inflation is trending down, and at this point, the Federal Funds Rate appears too restrictive; thus, the FED indicates that the rate will need to be cut several times next year, or they risk slowing the economy too much and potentially causing a recession. Thus far, the United States economy has been resilient, backed by a very strong labor market, sky-high job openings, low unemployment, and increasing consumer spending. Yet, storm clouds are gathering as consumer savings rates are at their lowest levels since 2009, excess savings from pandemic stimulus checks are running dry, and credit card debt has risen sharply. As a result, the economy is poised to cool. Mortgage rates drop with a subdued economy. This will result in a hotter housing market. When will housing heat up next year? It depends on when the economy cools. The forecast has three different scenarios: it cools during the spring, summer, or fall.

Scenario 1 – Economy Cools During the Spring (50% chance)

Scenario 2 – Economy Cools During the Summer (45% chance)

Scenario 3 – Economy Cools During the Fall (5% chance)

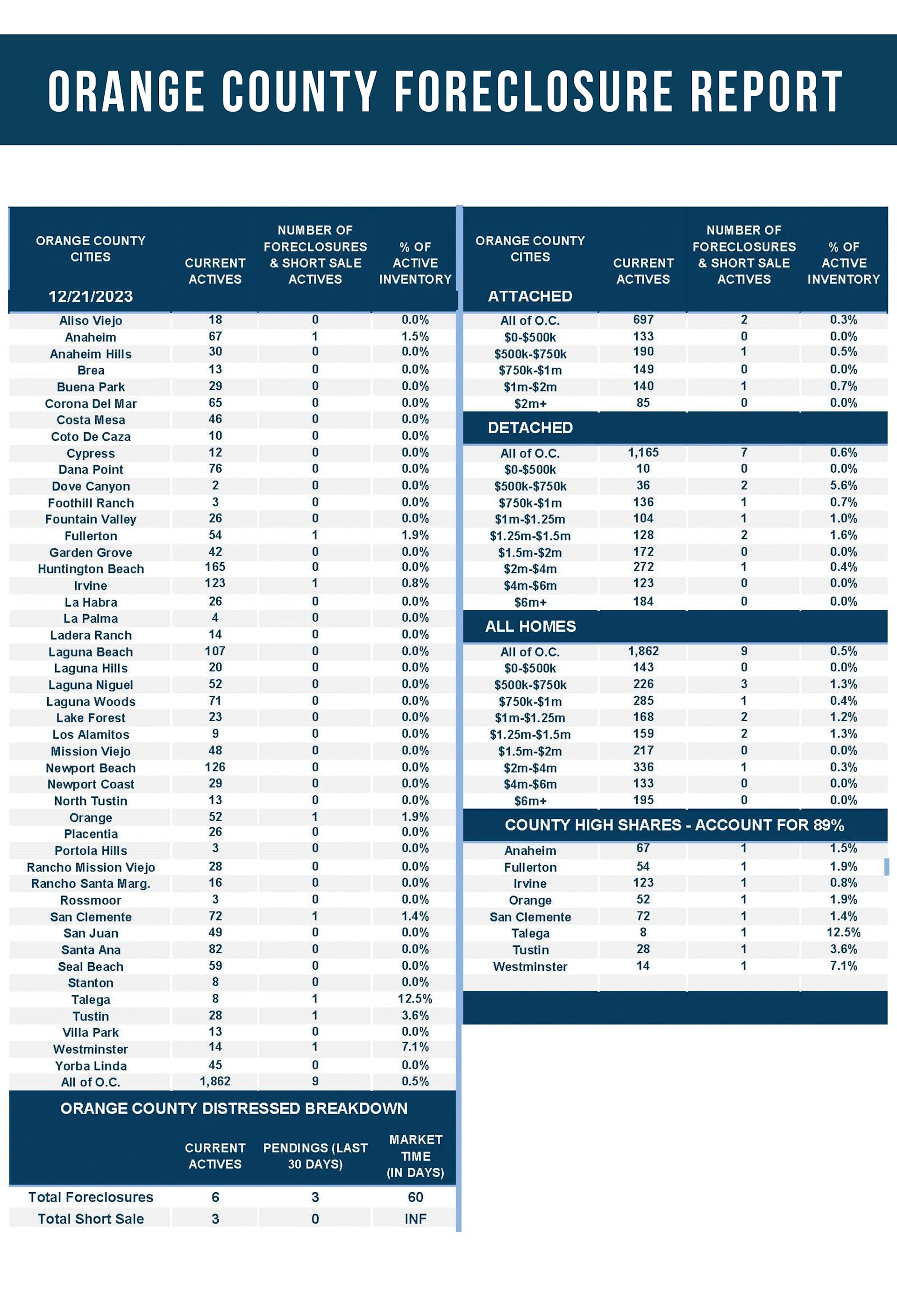

Additionally, the housing market will follow a typical housing cycle. Spring is the strongest in terms of demand, followed by the Summer Market, then the Autumn Market, and finally the Holiday Market. Luxury housing will be sluggish and will continue to transition to normal, longer market times, often taking months to procure a sale. The Spring Market will be the strongest for luxury and become sluggish and susceptible to Wall Street volatility during the year's second half. Finally, do not expect a wave of foreclosures and short sales. Distressed properties are still far below pre-pandemic levels, and homeowners are sitting on mountains of equity.

The bottom line is that the economy will cool sometime in 2024. When that occurs, rates will drop, and the housing market will heat up. No matter what, there will be more homeowners opting to sell their homes, pending sales will increase and surpass 2023 levels, and there will be more closed sales. How hot the housing market gets in 2024 depends upon when the overall economy downshifts.

Happy New Year!