As rates have edged higher and higher this year, the housing market has been slowing down from its insane pace, and now homes are taking a little longer to sell.

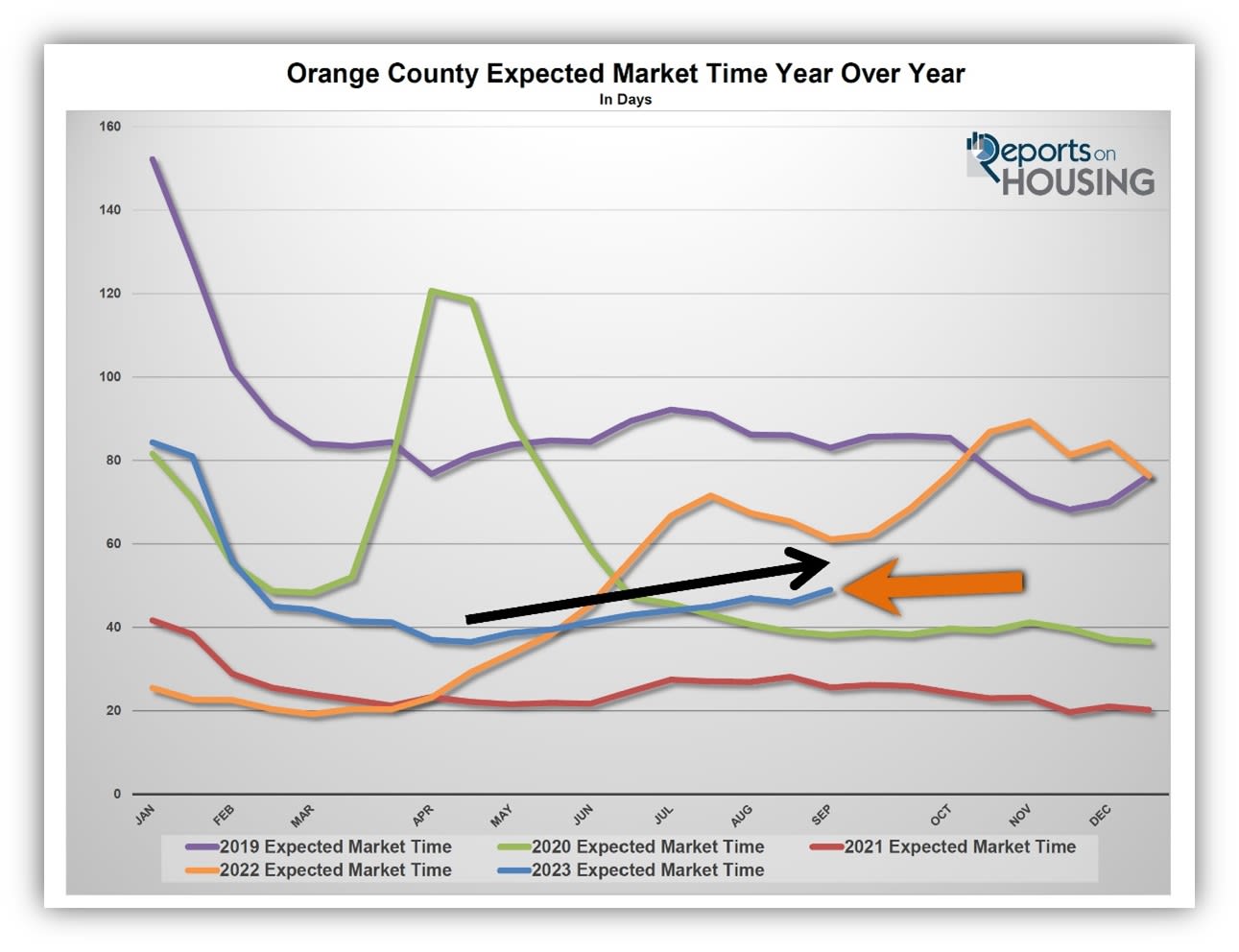

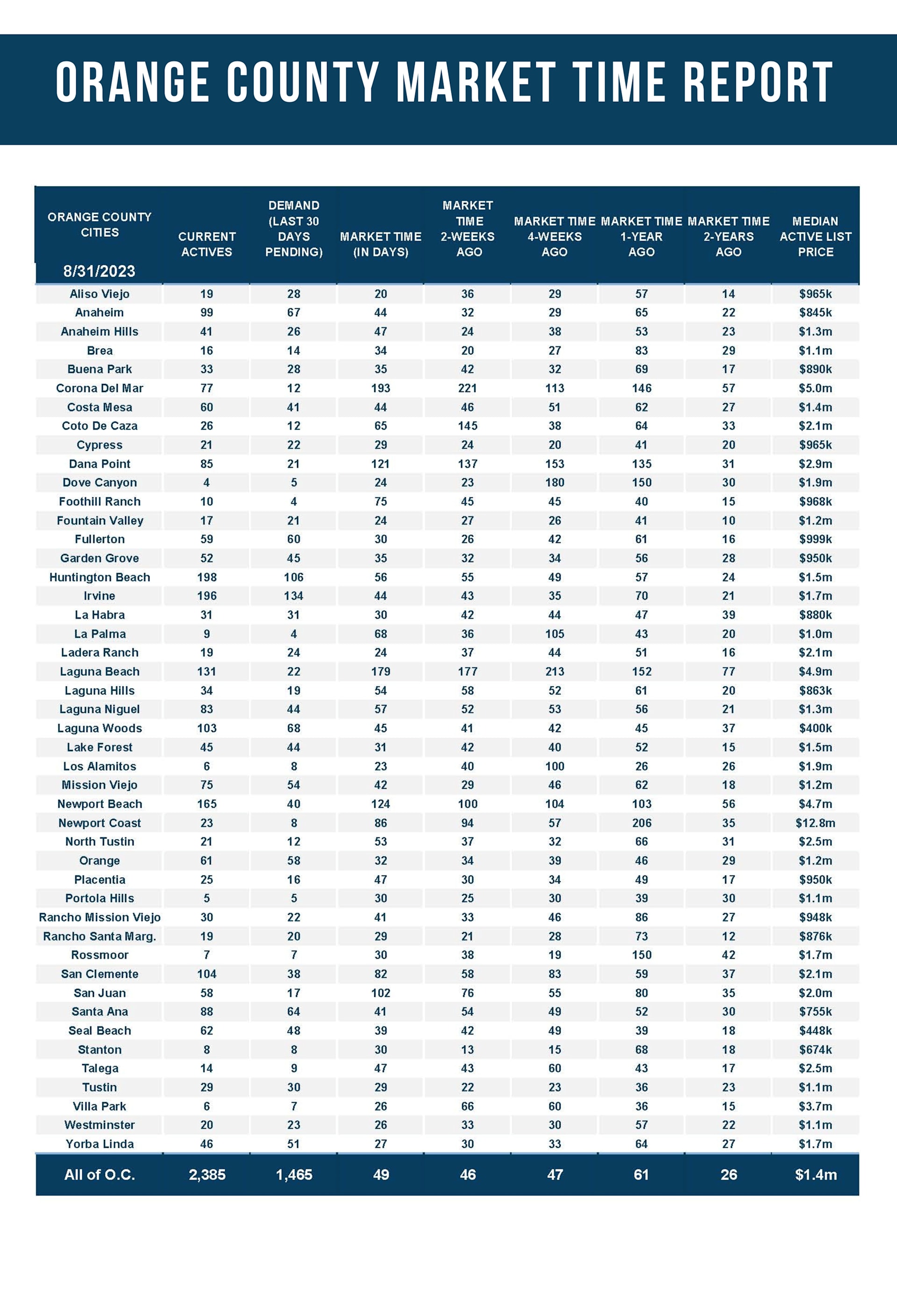

The Expected Market Time has grown from 37 days in April to 49 days today, a noticeable shift in the speed of the market due to rates rising above 7%.

It seems as if prices keep going up. Gas is once again above $5 per gallon. Date night at a favorite restaurant is now north of $100. A quick grocery stop for a few items totals more than $50. Wallets have been stretched. As a result, many are changing their spending habits and cutting back on extra errands or nights out.

Similarly, home affordability has been squeezed since the 30-year fixed rate climbed from 3.25% in January 2022 to over 7% in October and November 2022. This year started with mortgage rates easing to 5.99% in February. Yet, after reaching 6.39% in mid-April, they have been on the rise, climbing to 7.49% on August 21st, the highest mortgage rate according to Mortgage News Daily since December 2000, nearly 23 years ago. Buyers' wallets are stretched, and fewer and fewer can afford homes with these sky-high rates.

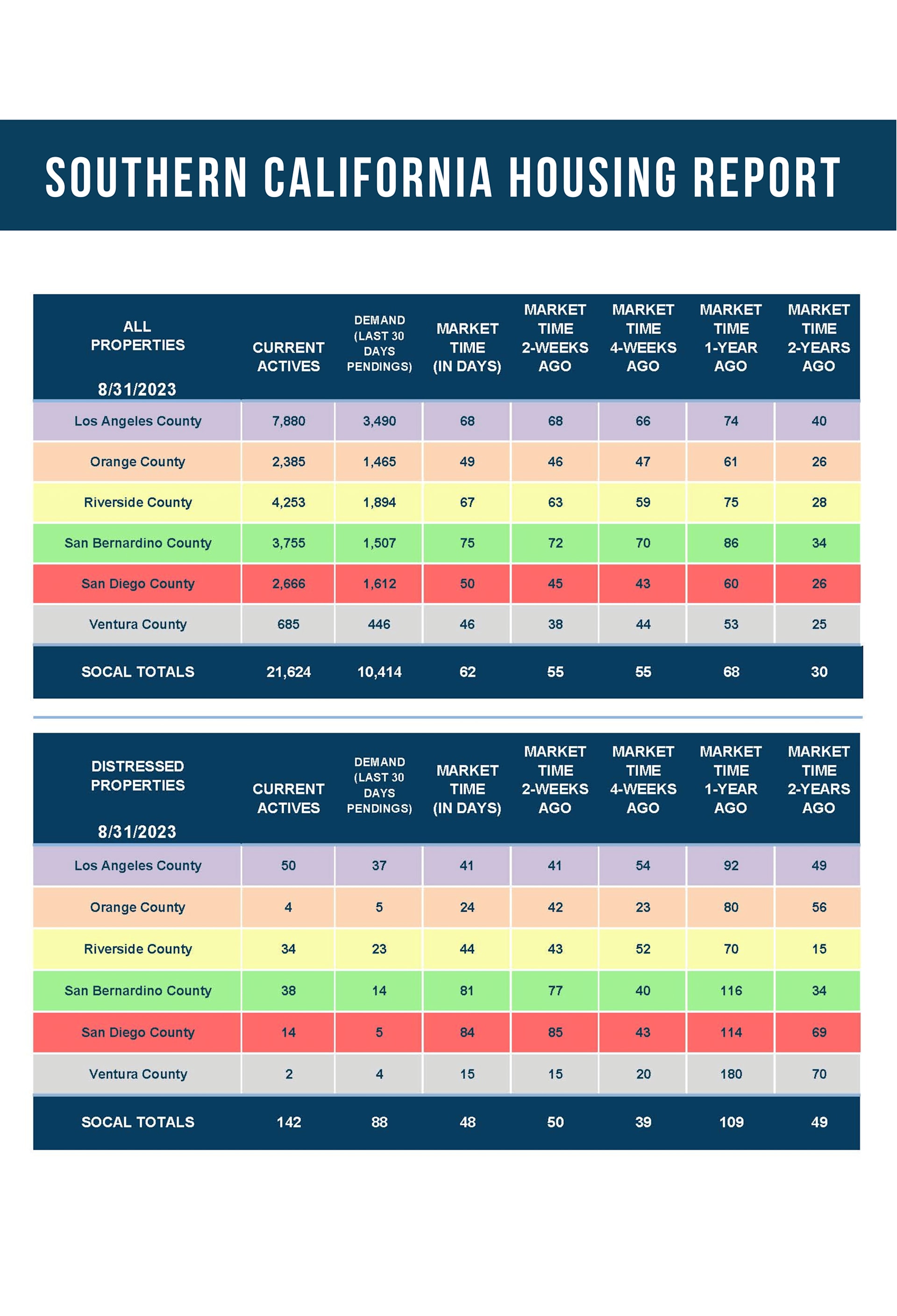

The Expected Market Time (the number of days to sell all Orange County listings at the current buying pace) reached its hottest reading of 2023 in April, just 37 days when rates had dropped to 6.16%. Slowly but surely, mortgage rates inched higher, eclipsing 7% in May. Demand remained flat, and the inventory increased little by little. The Expected Market Time rose slightly to 39 days, which is still remarkably hot. In June, rates hovered just below 7%, and demand did not change much, but the inventory continued its methodical, slow rise. The Expected Market Time climbed to 43 days. It was more of the same in July, and the market time climbed to 45 days. Last month, in August, as rates continued to spike, nearly reaching 7.5%, demand cooled further, and even though the inventory started to fall, the market time reached 49 days.

The market had gone from 37 days in April to 49 days in August, adding nearly two weeks to the market time. A market time of 49 days is still exceptionally fast and indicative of a “hot market” that favors sellers; yet, it also highlights the importance of careful pricing and having an approach to the market that is sympathetic to buyers pulling the trigger despite the high mortgage rate environment where affordability has been severely impacted. Price a home too high, and a seller will sit with no offers or low-ball offers to purchase. Homes that need a lot of work, deferred maintenance, lack upgrades, or have an unfavorable location will ultimately obtain less activity. They must adjust their price and expectations accordingly to secure a successful outcome.

According to economic experts in January, mortgage rates were anticipated to drop below 6% by the end of 2023. Instead, they have been on the rise. These experts have been forced to modify their outlook and now anticipate that they will remain higher for longer. The U.S. economy has been robust, with no recession in sight. Consumer spending has remained strong, and the job market has been exceptionally resilient with low unemployment, plenty of job openings, and increasing wages. Along with economists, the financial markets now believe that the Federal Reserve will keep rates higher until the second half of 2024 at the earliest. Consequently, mortgage rates have been rising.

Mortgage rates will eventually reverse course and start to decline as soon as there is evidence that the U.S. economy is weakening or inflation drops considerably. Unfortunately, many have learned that economics is slow and boring. It takes time for the economy to decelerate and for the job market to cool. Until then, expect mortgage rates to bounce around 7%, demand to remain muted, and market times to slowly decelerate. This will require sellers to be much more calculated in their approach to the housing market.

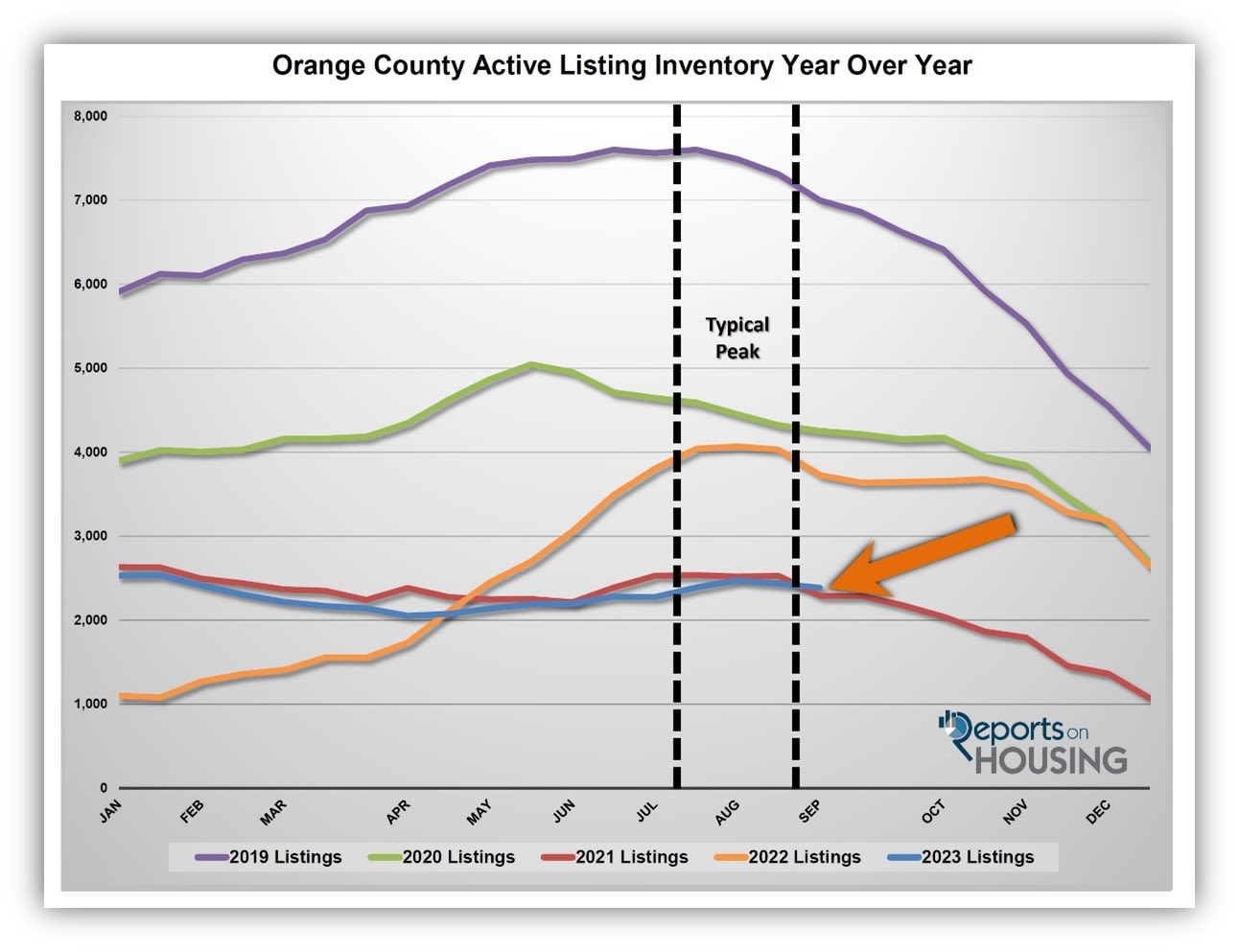

The active inventory decreased by 2% in the past couple of weeks.

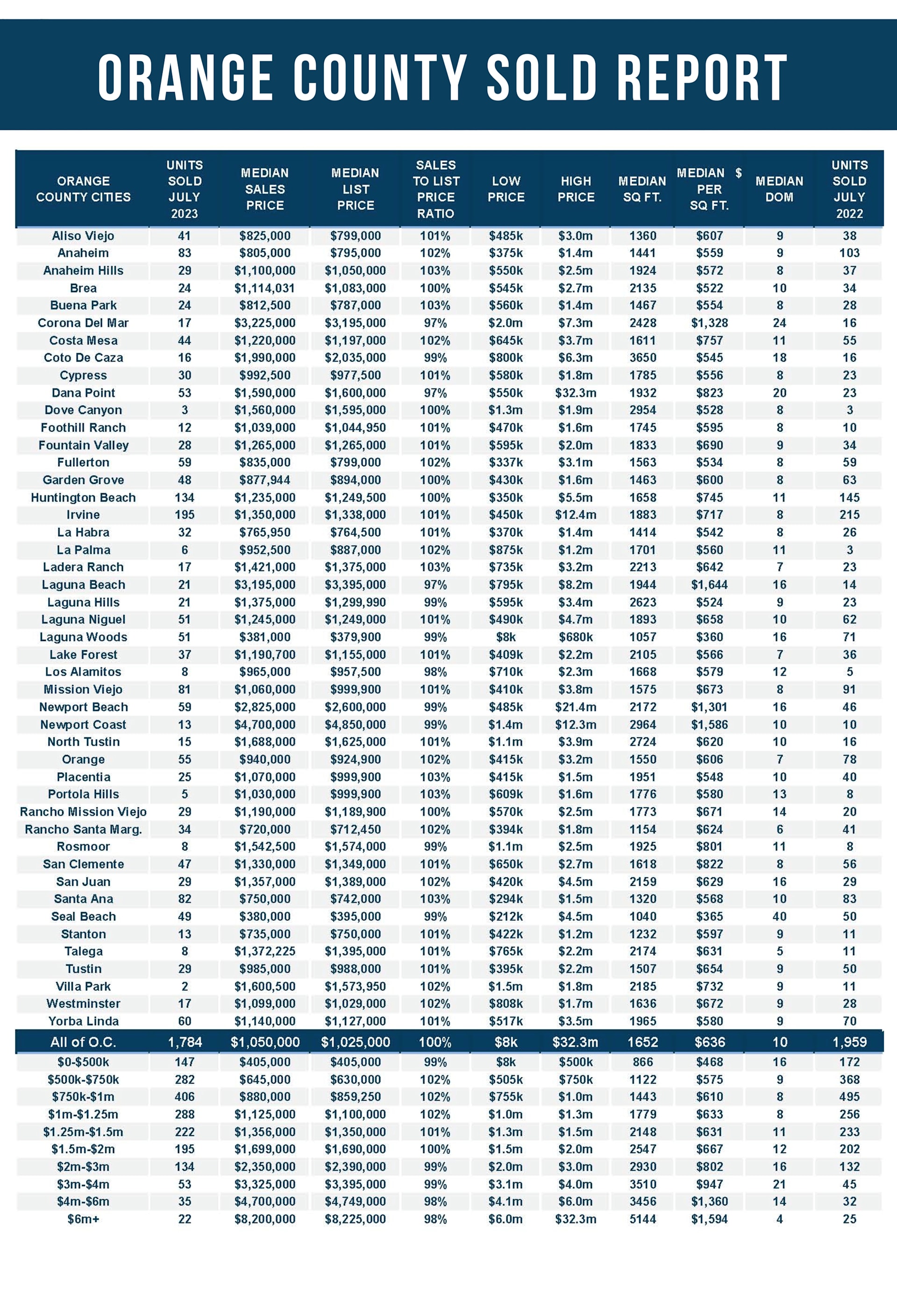

The active listing inventory decreased by 49 homes in the past two weeks, down 2%, and now sits at 2,385 homes, its lowest level since the start of July. For the first time this year, there are more homes than in 2021 to start September. Back then, it was the lowest level since tracking began in 2004. It now appears that the 2023 inventory peak was reached at the start of August at 2,475 homes, the lowest peak since tracking. From here, expect the inventory to slowly fall and closely mirror 2021. The inventory will plunge to complete the year during the holidays, from mid-November through New Year’s Day. Ultimately, this will set up a record-low number of available homes to start 2024.

Last year, the inventory was 3,726 homes, 56% higher, or 1,341 more. The 3-year average before COVID (2017 through 2019) is 6,569, an additional 4,174 homes, or 175% extra, nearly triple where it stands today.

Homeowners continue to “hunker down” in their homes, unwilling to move due to their current underlying, locked-in, low fixed-rate mortgage. For August, 2,170 new sellers entered the market in Orange County, 1,367 fewer than the 3-year average before COVID (2017 to 2019), 39% less. These missing signs counter any potential rise in the inventory.

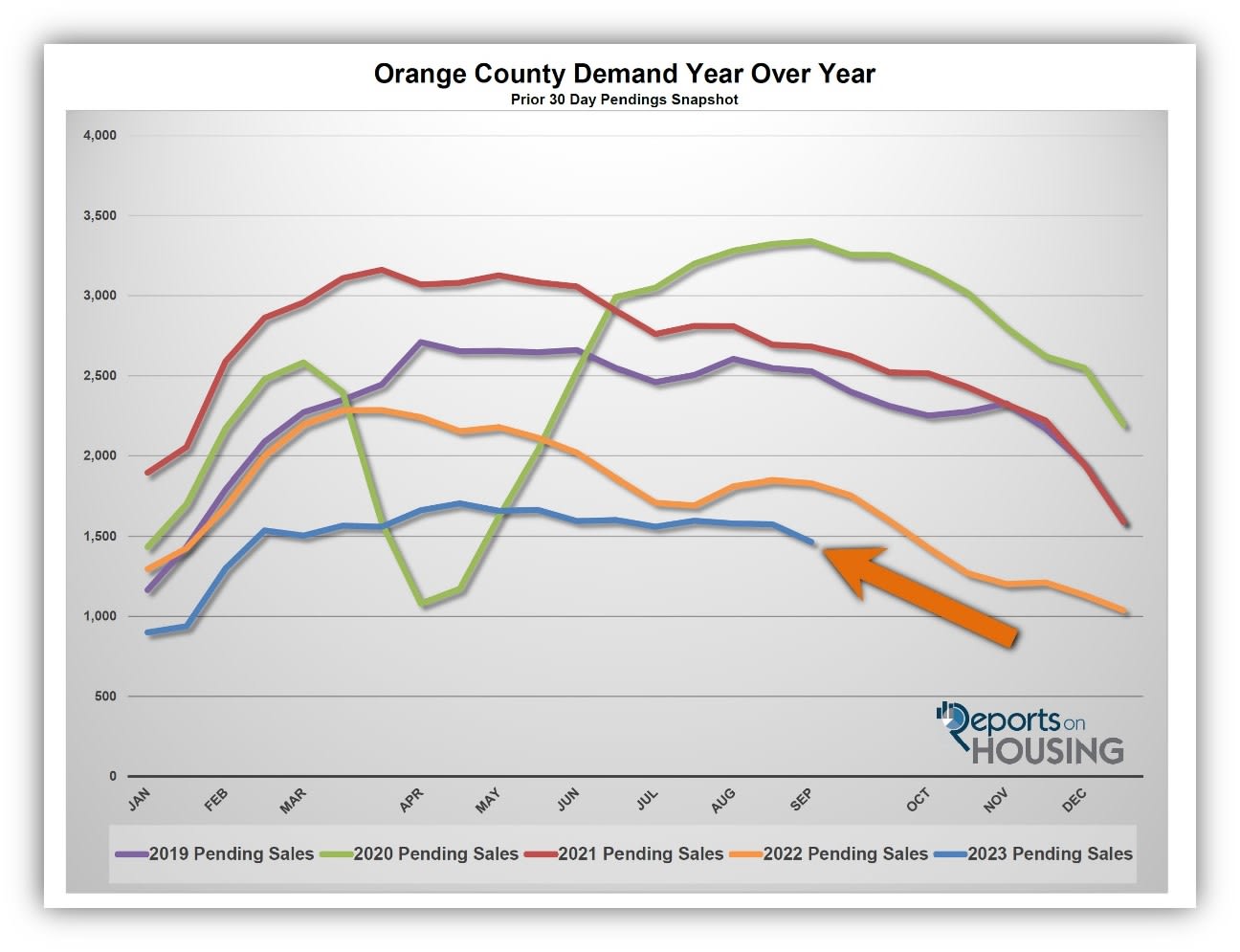

Demand plunged by 7% in the past couple of weeks.

Demand, a snapshot of the number of new pending sales over the prior month, plunged from 1,576 to 1,465 in the past couple of weeks, down 111 pending sales, or 7%, its largest drop of the year. The large decline coincides with mortgage rates reaching nearly 7.5% on August 22nd. As rates climb, fewer buyers qualify to purchase. Remember, both the Spring and Summer Markets are in the rearview mirror. Demand will continue to diminish slowly. During the holidays, from mid-November through the end of the year, demand will plunge along with the inventory.

Last year, demand was at 1,831, 25% more than today, or an extra 366. The 3-year average before COVID (2017 to 2019) was 2,438 pending sales, 66% more than today, or an additional 973.

With demand falling faster than supply, the Expected Market Time (the number of days to sell all Orange County listings at the current buying pace) increased from 46 to 49 days in the past couple of weeks, its highest level since the start of February. Last year, the Expected Market Time was 61 days, slower than today. The 3-year average before COVID was 82 days, significantly slower than today.

Luxury demand dropped by 21% in the past four weeks.

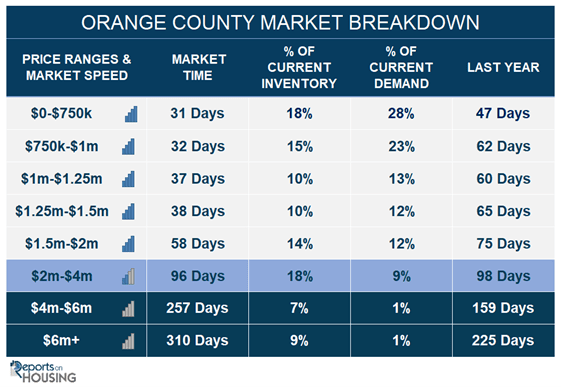

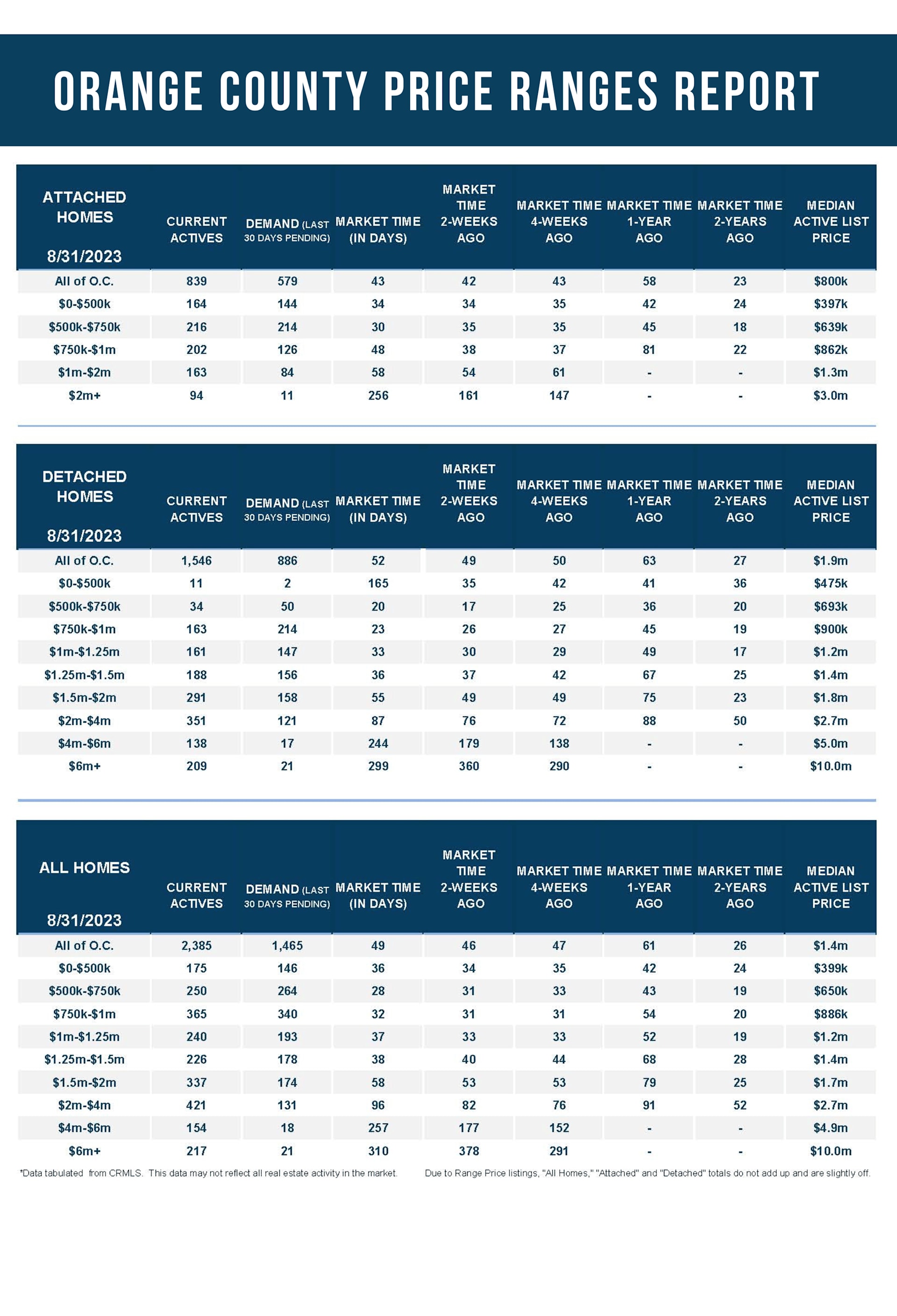

In the past couple of weeks, the luxury inventory of homes priced above $2 million decreased from 794 to 792 homes, down two, nearly unchanged. Luxury demand decreased by 26 pending sales, down 13%, and now sits at 170, the lowest level since the end of March. It has plunged by 21% as equity markets have concluded that the Federal Reserve will keep mortgage rates higher for longer. With supply unchanged and demand falling, the Expected Market Time for luxury homes priced above $2 million increased from 122 to 140 days. It was at 110 days just four weeks ago. Luxury sellers must have a calculated approach to the housing market, ignoring all the noise that the market is extremely hot in the lower ranges.

Year over year, luxury demand is down by 30 pending sales or 15%, and the active luxury listing inventory is up by seven homes or 1%. Last year’s Expected Market Time was 118 days, stronger than today.

For homes priced between $2 million and $4 million, the Expected Market Time in the past two weeks increased from 82 to 96 days. For homes priced between $4 million and $6 million, the Expected Market Time increased from 177 to 257 days. For homes priced above $6 million, the Expected Market Time decreased from 378 to 310 days. At 310 days, a seller would be looking at placing their home into escrow around July 2024.