With sky-high rates and a collapse in home affordability, many wrongly conclude that there will be a wave of foreclosures and it is just a matter of time before the housing market crashes.

Collectively, homeowners across the U.S. are healthier than ever before, which will prevent distressed sales and a housing crash.

Fear. Worry. Uncertainty. These words describe how many people feel about today’s housing market. Home values surged higher since 2022, and within the past couple of weeks, mortgage rates have climbed to heights not seen in 23 years. With home affordability at record lows, many argue that when the economy cools or slips into a recession, housing will collapse, and foreclosures will rise. After all, isn’t that how the Great Recession unfolded?

The general public often jumps to conclusions without looking at all the facts and trend lines. They remember the burn from 2008 through 2011. Everybody was burned or knew someone hurt by the collapse in home values. The economy ground to a halt, and unemployment grew to levels last seen at the beginning of the 1980s. Thus, everyone is jumping to the worst-case scenario in their collective minds: housing must suffer.

It is imperative to immediately point out that just because mortgage rates have climbed towards 8% does not mean that values must go down, and many homeowners will lose their homes due to foreclosures or short sales. The Great Recession was fueled by a credit bubble inflated by loose lending standards, including subprime mortgages, pick-a-payment plans, teaser adjustable rates, zero down, and plenty of fraud. These high risk borrowers were susceptible to any adjustments in their rates or changes to the economy. Thus, a wave of foreclosures ensued.

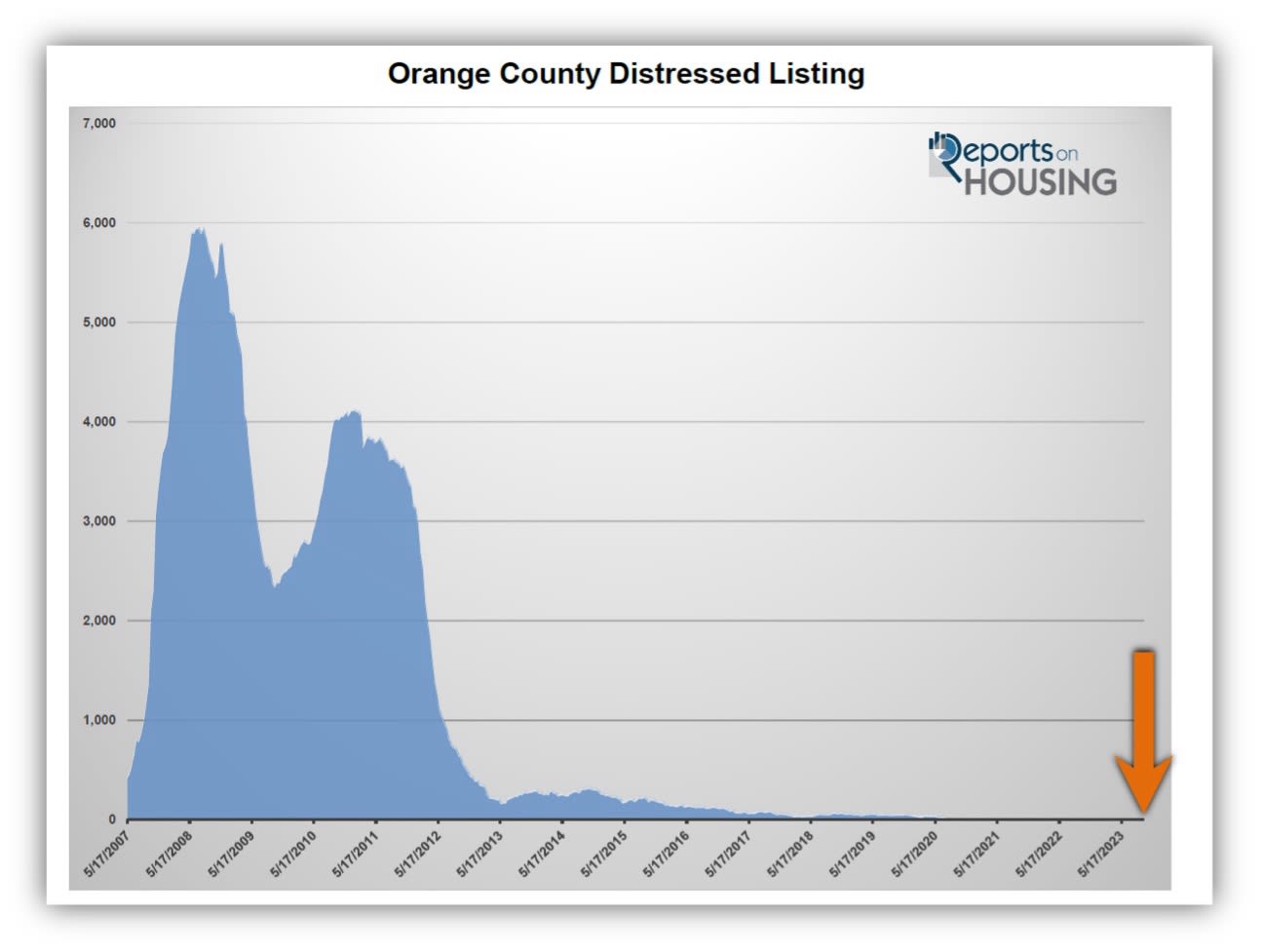

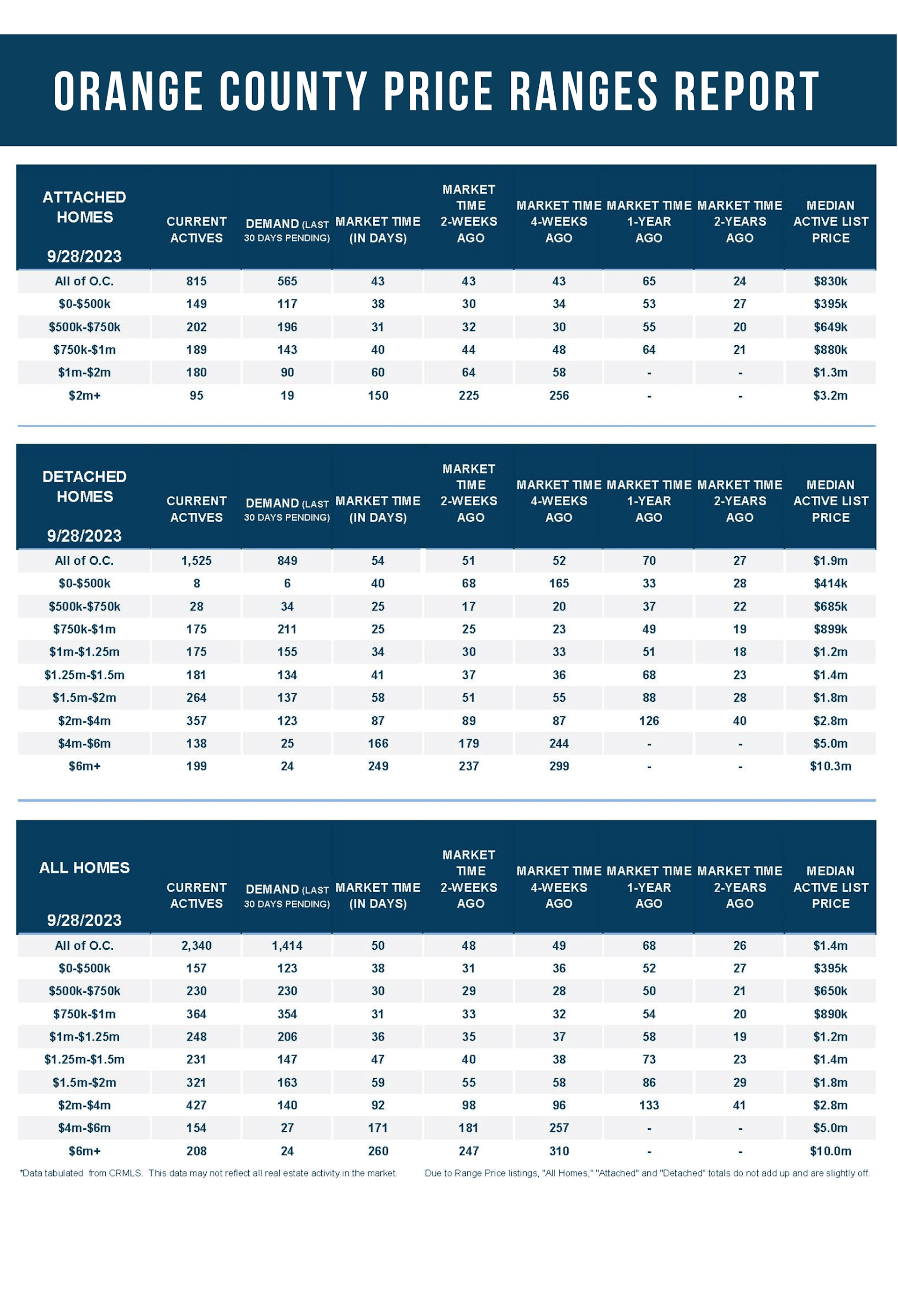

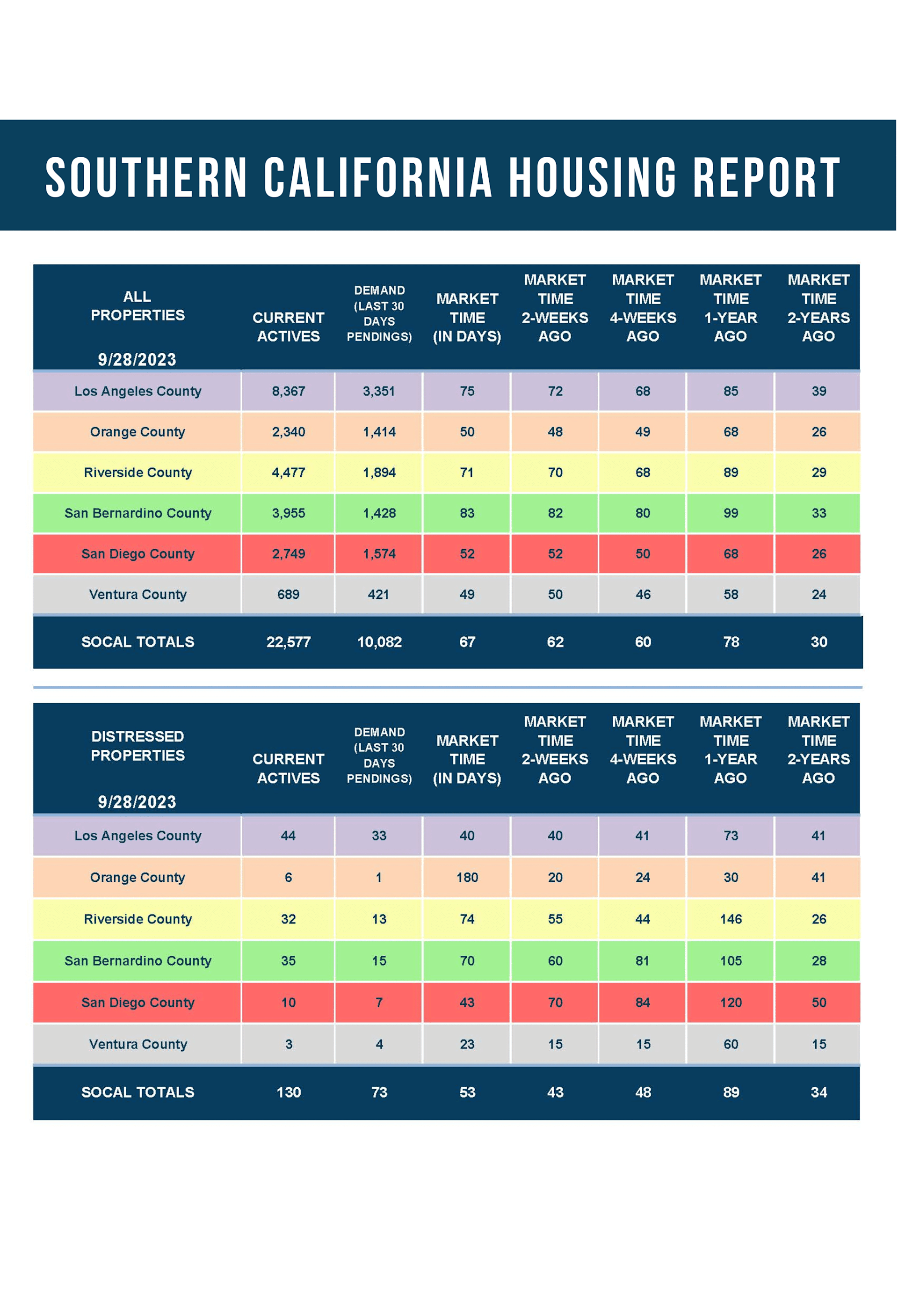

Today, only four foreclosures and two short sales are available to purchase in Orange County; that is only six total distressed listings. Distress demand, the number of new pending sales over the prior month, is at one. Foreclosures and short sales represent only 0.3% of the active listing inventory and 0.07% of overall demand. Compare that to January 2009, when there were 5,104 distressed listings, 44% of the inventory, and distressed demand was at 1,428 pendings, 67% of total demand.

That is correct. Two-thirds of demand was distressed. Lenders were in control of the housing market through bank-owned listings, foreclosures, and short sales, where the lender (or lenders) needed to approve taking less than the outstanding loan balance. They were unemotional sellers willing to do whatever it took to sell. Often, that meant pricing a home below the most recent closed sale. Consequently, home values plummeted.

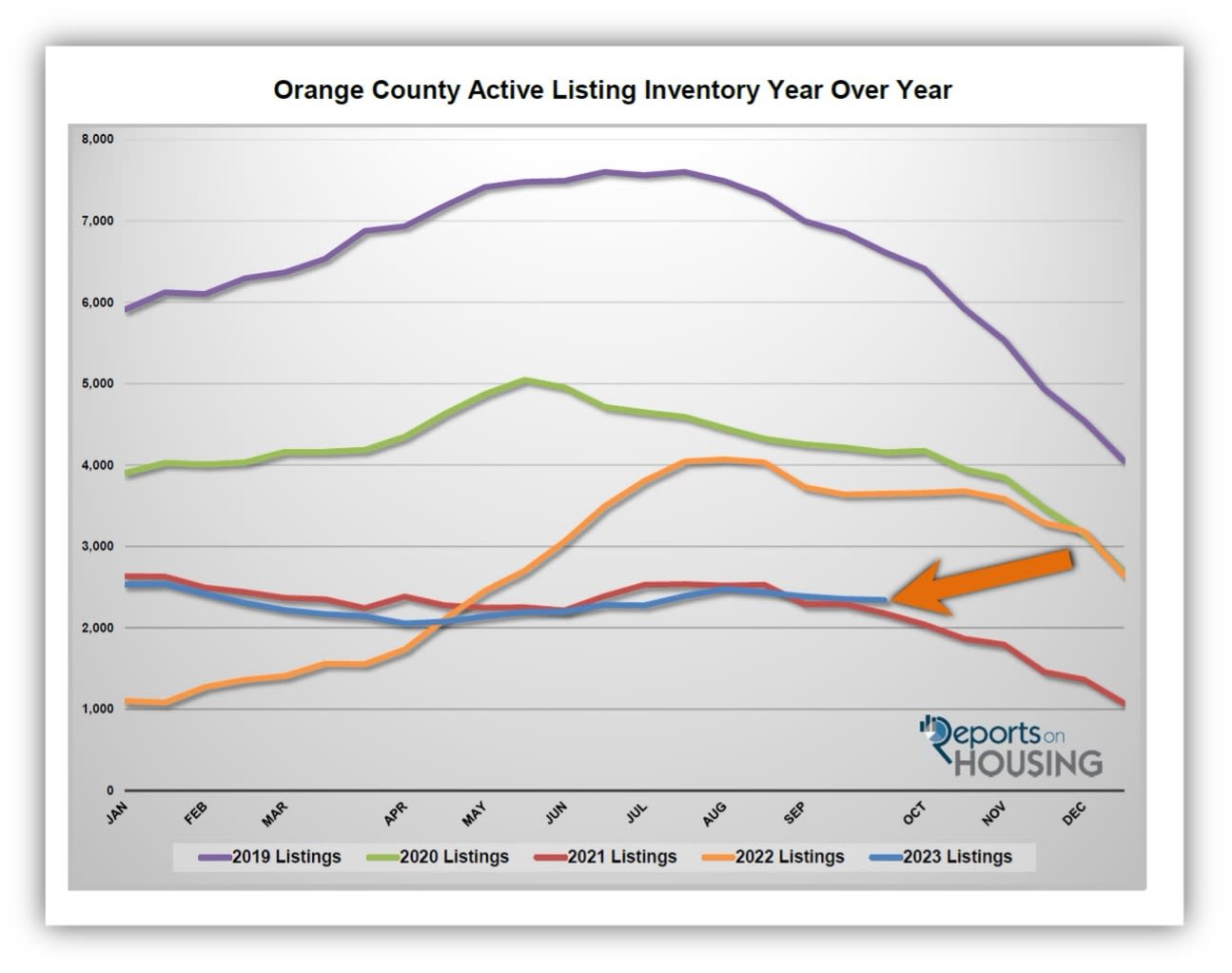

Some believe right now is the calm before the storm, similar to 2005 through 2006. Yet, this is where today’s catastrophically low inventory and the strength of the homeowner step in and squash this argument. The leadup to the Great Recession was characterized by an Orange County inventory that grew from 4,900 homes in March 2005 to over 16,000 homes in the summer of 2006, a glut of homes for sale. This year, the inventory climbed to 2,475 homes and will drop to around 1,500 by year’s end, nearly a record low.

Before the Great Recession, the average buyer FICO score was 681 (2006), low or no-down-payment loans were common, and buyers tapped into subprime mortgages, pick-a-payment plans, and teaser adjustable-rate products. Adjustable-rate mortgages made up over a third of mortgage applications each year from 2004 to 2007. There was a flood of cash-out refinances where homeowners used their homes like ATMs. When the economy slipped into a recession and adjustable-rate mortgages reset to much higher rates, a wave of homeowners could no longer afford to make their monthly payments. Increasing unemployment surged from 5% in January 2008 to 10% in 2009, exacerbating an already stressed housing stock.

Today’s housing stock is entirely different. Lending has been tight ever since the adoption of the Dodd-Frank Act of 2010, a law that provided common-sense protections for consumers in obtaining a loan. Buyers have purchased homes with higher down payments, tight qualification and lending standards, and an average FICO score of 746 (2022). Cash-out refinances are at their lowest levels since 2000. Unemployment has remained at decade lows, below 4%. An incredible 96% of homeowners with a loan enjoy low fixed-rate mortgages. Unlike before and during the Great Recession, homeowners today are not vulnerable to rising payments. Nearly 50% of all homeowners across the county are considered “equity rich,” meaning they have more than 50% equity in their homes.

Homeowners do not have to move. They have qualified for years with solid credit and good jobs and are now enjoying their low, fixed payments. Consequently, homeowners continue to “hunker down” in their homes, unwilling to move due to their current underlying, locked-in, low rate. According to the Federal Housing Finance Agency’s National Mortgage Database, 85% of Californians with a mortgage have a rate of 5% or lower, 69% is 4% or lower, and 30% is 3% or lower. As a result, fewer homeowners are listing their homes for sale in the current high-rate environment. From January through September, 18,653 new sellers entered the market in Orange County, 13,760 fewer than the 3-year average before COVID (2017 to 2019), 42% less. These missing signs exacerbate the low inventory dilemma and have led to a waterfall dive in the number of closed sales.

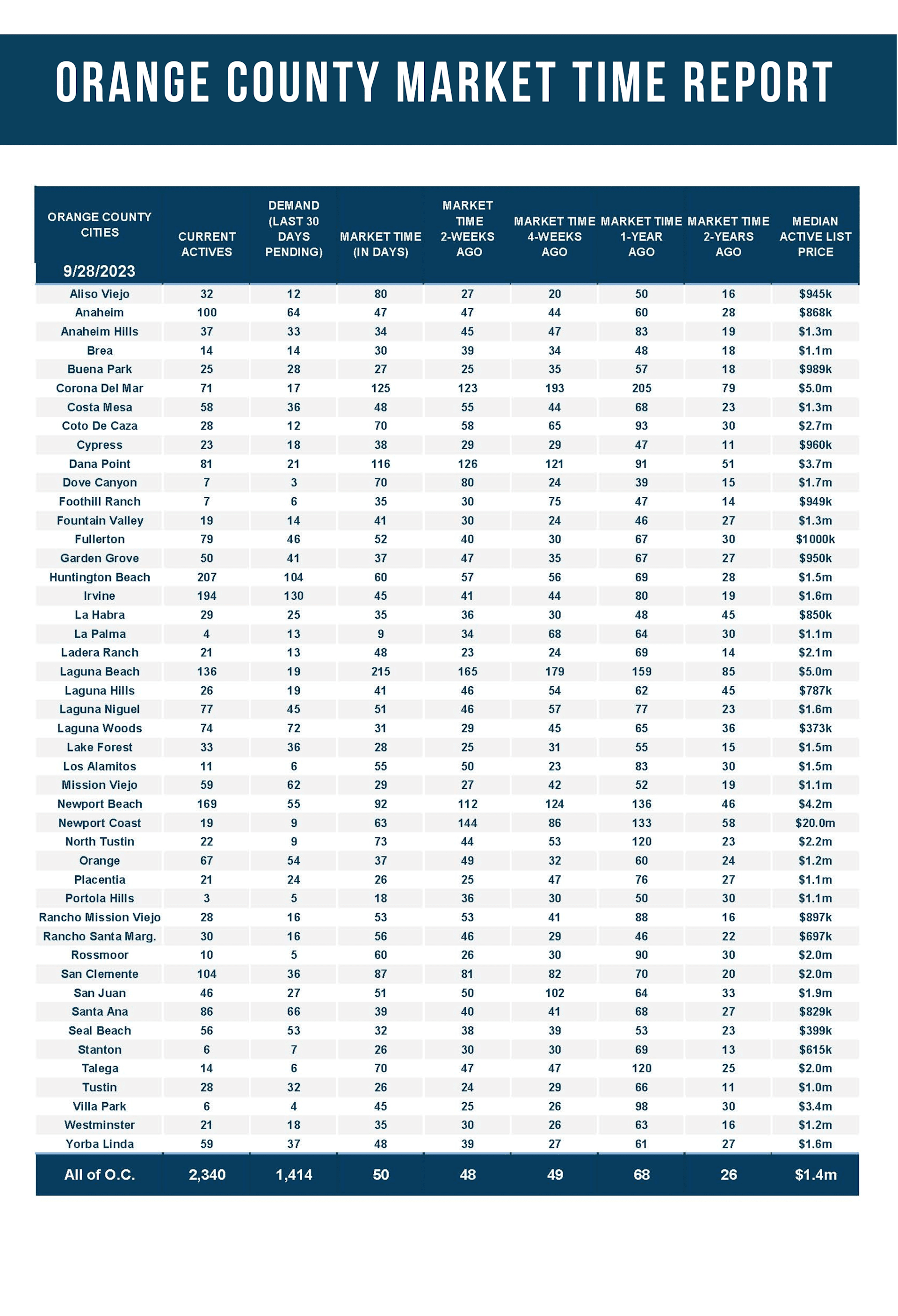

The bottom line: do not count on a wave of distressed homes or a housing crash. The Orange County Expected Market Time (the number of days to sell all listings at the current buying pace) is at 50 days, lower than last year’s 68-day level and much stronger than the 3-year average prior to COVID at 86 days. Even if the market were to line up slightly favoring buyers in the negotiating process, the inventory crisis and strong housing stock would prevent a substantial downturn.

The active inventory decreased by 1% in the past couple of weeks.

The active listing inventory decreased by 13 homes in the past two weeks, down 1%, and now sits at 2,340 homes, its lowest level since the start of July. It is the second lowest level since tracking began in 2004, behind 2021, with 161 additional homes. Even though Orange County has already peaked, it has not dropped much, shedding only 135 homes in the past eight weeks. The inventory level is sticky and not dropping faster because of sky-high rates that have recently surged higher, eroding home affordability. Rates have been higher than 7% since the end of July and have recently eclipsed 7.5%, the highest mortgage rate since 2000. The deterioration in affordability has placed even more pressure on demand. Accordingly, the active inventory has remained flat. Expect the inventory to continue to slowly fall until mid-November, the start of the Holiday Market. From there, it will plunge through New Year’s Day.

Last year, the inventory was 3,646 homes, 56% higher, or 1,306 more. The 3-year average before COVID (2017 through 2019) is 6,400, an additional 4,060 homes, or 173% extra, nearly triple where it stands today.

Homeowners continue to “hunker down” in their homes, unwilling to move due to their current underlying, locked-in, low fixed-rate mortgage. For September, 1,915 new sellers entered the market in Orange County, 1,114 fewer than the 3-year average before COVID (2017 to 2019), 37% less.

Demand decreased by 4% in the past couple of weeks.

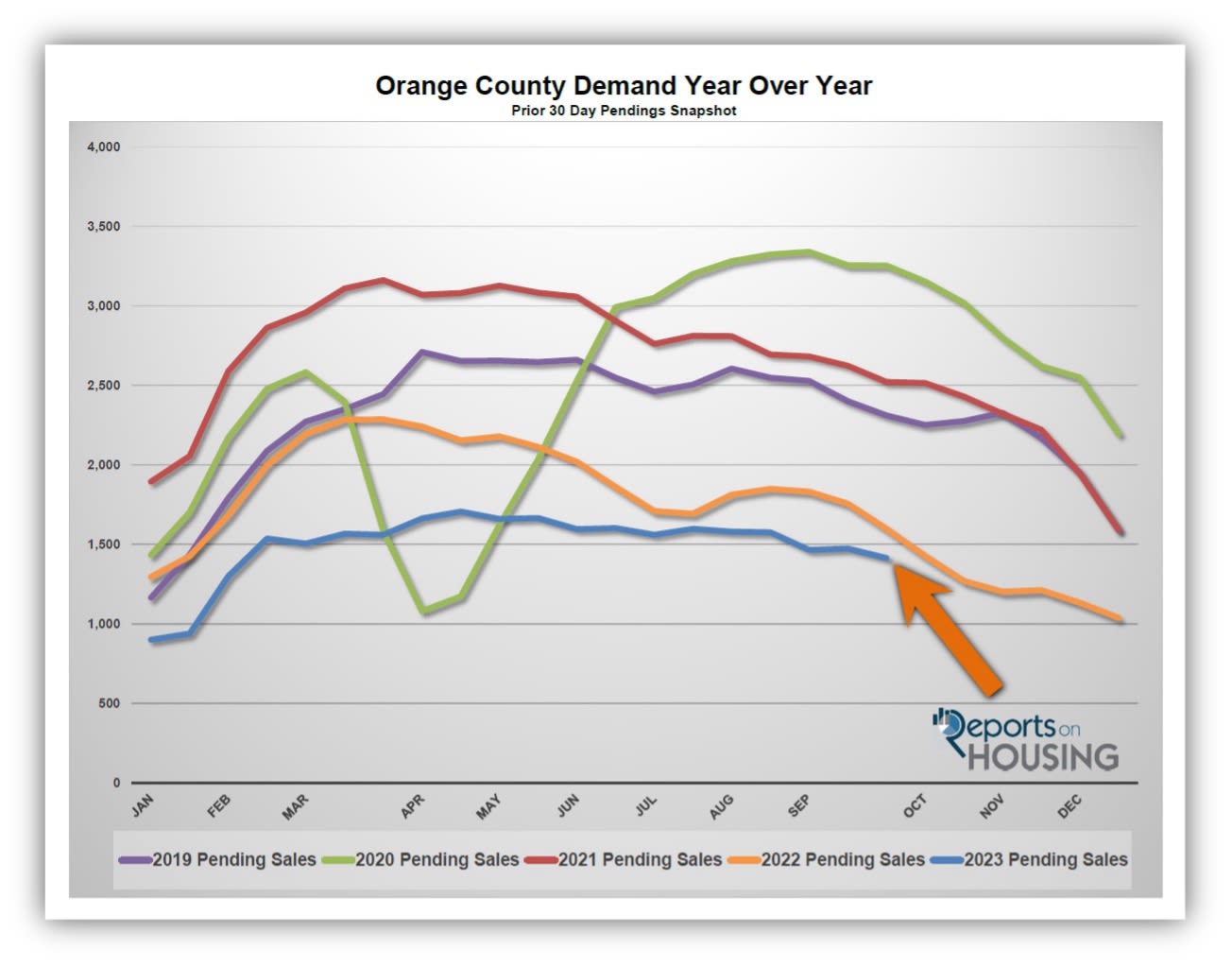

Demand, a snapshot of the number of new pending sales over the prior month, decreased from 1,474 to 1,414 in the past couple of weeks, down 60 pending sales, or 4%, its lowest level since the start of February. It is the lowest September reading since 2007. With mortgage rates stuck above 7% and now hitting new 2023 highs, there is more and more pressure on pricing as more potential buyers are priced out of the market. Home affordability impacts demand. As rates rise, fewer can afford to buy. When rates fall, more buyers enter the market. Until rates drop below 7%, expect demand to remain at muted levels. For the remainder of the year, demand will slowly diminish and will drop at a faster rate during the holiday season.

With demand dropping faster than supply, the Expected Market Time (the number of days to sell all Orange County listings at the current buying pace) increased from 48 to 50 days in the past couple of weeks, its highest level since the end of January. Last year, the Expected Market Time was 68 days, slower than today. The 3-year average before COVID was 86 days, significantly slower than today.

The luxury market has improved a bit in the past couple of weeks.

In the past couple of weeks, the luxury inventory of homes priced above $2 million decreased from 798 to 789 homes, down nine, or 1%. Luxury demand increased by eight pending sales, up 4%, and now sits at 191. With demand climbing and the supply falling slightly, the Expected Market Time for luxury homes priced above $2 million decreased from 131 to 124 days. Yet, at 124 days, luxury sellers must still have a calculated approach to the housing market, ignoring all the noise that the market is hot in the lower ranges.

Year over year, luxury demand is up by 46 pending sales or 32%, and the active luxury listing inventory is down by eight homes or 1%. Last year’s Expected Market Time was 165 days, slower than today.

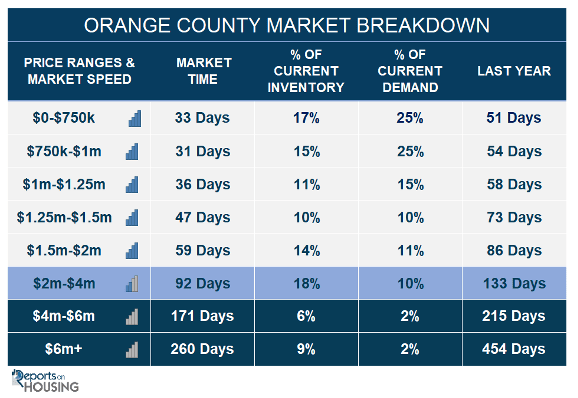

For homes priced between $2 million and $4 million, the Expected Market Time in the past two weeks decreased from 98 to 92 days. For homes priced between $4 million and $6 million, the Expected Market Time decreased from 181 to 171 days. For homes priced above $6 million, the Expected Market Time increased from 247 to 260 days. At 260 days, a seller would be looking at placing their home into escrow around June 2024.